RESOURCES

Resources

When a productive hourly worker becomes disengaged or suddenly quits, it can adversely impact your business. Discover ways to hang on to your top employees.

A prominent New Jersey couple faces allegations that they invested plan assets in companies in which they had significant financial interest and in ways that would personally benefit them.

The body content of your post goes here. To edit this text, click on it and delete this default text and start typing your own or paste your own from a different source.

It’s not too late to get clients ready for 2023

Close to half of U.S. private-sector employees ages 18 to 64 work for a company that doesn't offer either a traditional pension or a retirement savings plan.

Unions don’t just protect the financial security of workers while they are on the job. They also work hard to ensure the financial security of workers after they retire. As the American Federation of Labor and Congress of Industrial Organizations (AFL-CIO) notes, “Unions of working people advocate for strong pensions, expanded Social Security benefits and adequate wages so people can build up retirement savings over the course of their careers.” They accomplish this by negotiating retirement benefits into collective bargaining agreements and lobbying lawmakers to protect worker retirement benefits. Because of the advocacy, union workers are more likely than nonunion workers to have retirement benefits. According to 2020 data from the Bureau of Labor Statistics , 91 percent of union workers had access to a retirement plan compared to only 65 percent of nonunion workers. Unions Negotiate Pension Plans Into Contracts Pension plans are one of the many benefits unions negotiate into collective bargaining agreements. Most of those plans are defined benefit plans, which means workers get a guaranteed, specified benefit from their employer upon retirement. Many of these plans, like the CWA/ITU NPP (Negotiated Pension Plan) , are also multiemployer pension plans designed for workers who change employers often within their industries throughout their careers. They are most common in unionized industries like retail, construction, manufacturing, and transportation. Such plans ensure that workers don’t lose out on retirement benefits as they move from one employer to another. Multiemployer pension plans are negotiated between unions and employers who agree to fund the accounts. Contribution amounts for each employer are negotiated during collective bargaining. Those employer contributions go into trust funds run by trustees selected by the union and the employers. By including these contributions in contracts, unions ensure workers have the financial means they need to support themselves in retirement. Unions Lobby Lawmakers for Legislation That Protects Worker Retirement Labor leaders also advocate for retirement protections for workers, two of which have to do with Social Security expansion and the Emergency Pension Plan. Expanding Social Security Unions were instrumental in the creation of the federal Social Security program and continue to advocate for expanding the benefits to retirees offered by the program. According to the Service Employees International Union (SEIU) , strengthening Social Security is important because it’s the primary source of income for most retired Americans and expanding it would ensure benefits keep up with inflation. That’s why the International Federation of Professional & Technical Engineers (IFPTE) and other labor organizations are lobbying for the passage of the Social Security 2100 Act . “It is critical that now more than ever we make sure our Social Security system will be there to help our nation withstand what could be a retirement crisis in the very near future,” write IFPTE’s Matthew S. Biggs and Gay Henson in a letter of support. Pension Plan Relief When lawmakers were drafting and debating President Biden’s COVID relief bill — The American Rescue Plan — earlier this year, unions successfully lobbied to have the Butch Lewis Emergency Pension Plan Relief Act of 2021 included in the package. This legislation was a priority for unions because it restores the solvency of more than 100 at-risk multiemployer pension plans which provide benefits to more than one million people. “In this dire situation, the cost of inaction is far greater than the cost of this sensible legislative solution,” Robert Martinez, Jr. , president of the International Association of Machinists and Aerospace Workers (IAM), wrote in a letter to the House Ways and Means Committee supporting the bill’s inclusion in the American Rescue Plan. The efforts of the IAM and others paid off when the Pension Plan Relief Act was included in the relief package, ultimately ensuring workers and retirees can keep the retirement they have earned. “The retirees will keep 100% of their benefits and no cuts. This is a phenomenal achievement,” said Bob Amsden , a retired International Brotherhood of Teamsters member in Wisconsin. As union leaders continue to fight to protect the financial security of workers in retirement, a tool like UnionTrack ENGAGE can help them update members regarding their negotiation and lobbying progress.

Defined contribution retirement plan participants have continued to save for retirement in the face of economic uncertainty caused by the COVID-19 pandemic, according to information collected in the new Vanguard report “How America Saves 2021.” Amber Brestowski, principal and head of advice and client experience for Vanguard’s institutional investor group, says that this year the annual report shows that plan sponsors continue to support participants’ progress toward retirement preparedness. “Plan sponsors are using smart plan design to get participants enrolled in retirement plans and saving at higher rates,” she says. “DC plan sponsors are rising to the occasion [and] ensuring that their participants are retirement ready. We also acknowledge the game is changing. Employees’ expectations are increasing and that’s something that the Vanguard plan sponsors that we serve are watching and responding to.” The Retirement Road Vanguard’s survey found that participants’ median total contribution rate—including participant and employer contributions—was 10.4% in 2021, compared to 10.5% in 2020. Vanguard credits plan sponsors adopting automatic deferral and automatic escalation for the rate staying steadfast through the pandemic, market volatility and spiking inflation. Nonetheless, roughly half of retirement plan participants continue to save below the recommended savings rate of 12% to 15% of their salary, the data shows. Vanguard found that slight deferral increases could help close this savings gap, as about 20% of participants saving below these levels are just 1-3% away from the target savings rate. Brestowski adds that plan sponsors and participants have slogged through challenges in the last two years, including increased financial stress at work, that have heavily affected retirement readiness, while more than 70% of Americans say anxiety over finances is their top stressor. “The pandemic shone a bright light on the unstable position of most Americans’ finances,” she says. “[Workers] are looking to their employer to help them with their financial well-being and at the same time, there’s a war for talent, [with] some of the tightest labor markets that we’ve seen in recent history, so employers also know that anxiety over finances jeopardizes an employee’s path to a successful retirement and impacts day-to-day lives.” She adds that employers know that to attract and retain the best talent, they must help employees live their best financial lives. “We see more and more employers spreading their focus beyond retirement to help employees manage their plethora of financial needs,” Brestowski says. Adding Advice Plan sponsors are meeting the demand with financial wellness benefits—including tools and resources for participants to address their overall financial picture—alongside retirement plans. Plan sponsors are also increasingly offering access for employees to support their investment acumen and retirement readiness, she adds. For example, 41% of all Vanguard DC plans offered managed account advice in 2021 and almost 80% of large plans offered the service. In 2021, the percentage of participants who were offered managed account advice was 74% and the percentage of participants who were offered managed account advice and accessed the service was 10%. In 2017, the percentage of plans offering managed account advice was 30%, while the percentage of participants offered managed account advice was 55% and the percentage of participants who were offered managed account advice and used the service was 7%, Vanguard finds. Participant and Plan Sponsor Progress David Stinnett, principal and head of strategic retirement consulting at Vanguard, highlights data from the survey that he says shows continued ”forward progress” for retirement investors. The report shows that 2% of participants stopped contributing to retirement plans in 2021, and 7% of participants decreased their salary deferrals compared to figures from 2019 and 2020. In 2021, 17% of participants made a participant-directed increase, 25% made an increase due to auto-escalation and 49% made no change. “You could be excused for thinking, with a year like that, ‘Maybe we won’t see forward progress, maybe we’ll see things halt or even reverse given all the exogenous factors in the market,’” Stinnett says. “And I was just delighted to see that that was not the case.” In 2020, 9% of participants made no change, 2% made an increase due to auto-escalation, 16% made a participant-directed increase, 8% made a participant-directed decrease and 2% stopped contributing. Vanguard found that the estimated participation rate for DC plans was 85% in 2021, compared to 78% in 2012. The participation rate for plans that used auto-enrollment in 2021 was 93%, compared to 66% for plans that did not use auto-enrollment. In 2021, 58% of plan sponsors using auto-enrollment increased the default contribution rate to 4% or higher, Stinnett adds. “[Research shows] not only higher participation rates year over year, but a very stark difference between those plans that have automatic enrollment and those plans which do not,” he says. Another signal that participants continued to save: retirement investors’ account trading activity was muted in 2021, Vanguard found. Among Vanguard DC plan participants, 8% traded within their accounts and 9% did not make any changes to their investments. “The decline in participant trading is partially attributable to participants’ increased adoption of target-date funds,” the report states. “Only 3% of participants holding a single target-date fund traded in 2021.” Participants have also preserved their assets for retirement. In 2021, about 25% of participants could have taken an account distribution because of a job separation, yet 83% of that group continued to preserve their plan assets for retirement by either remaining in the employer’s plan or rolling over the savings to an individual retirement account or a new employer’s plan. “In terms of assets, 98% of all plan assets available for distribution were preserved and only 2% were taken in cash,” the report states.

INDUSTRY TRENDS AND RESEARCH

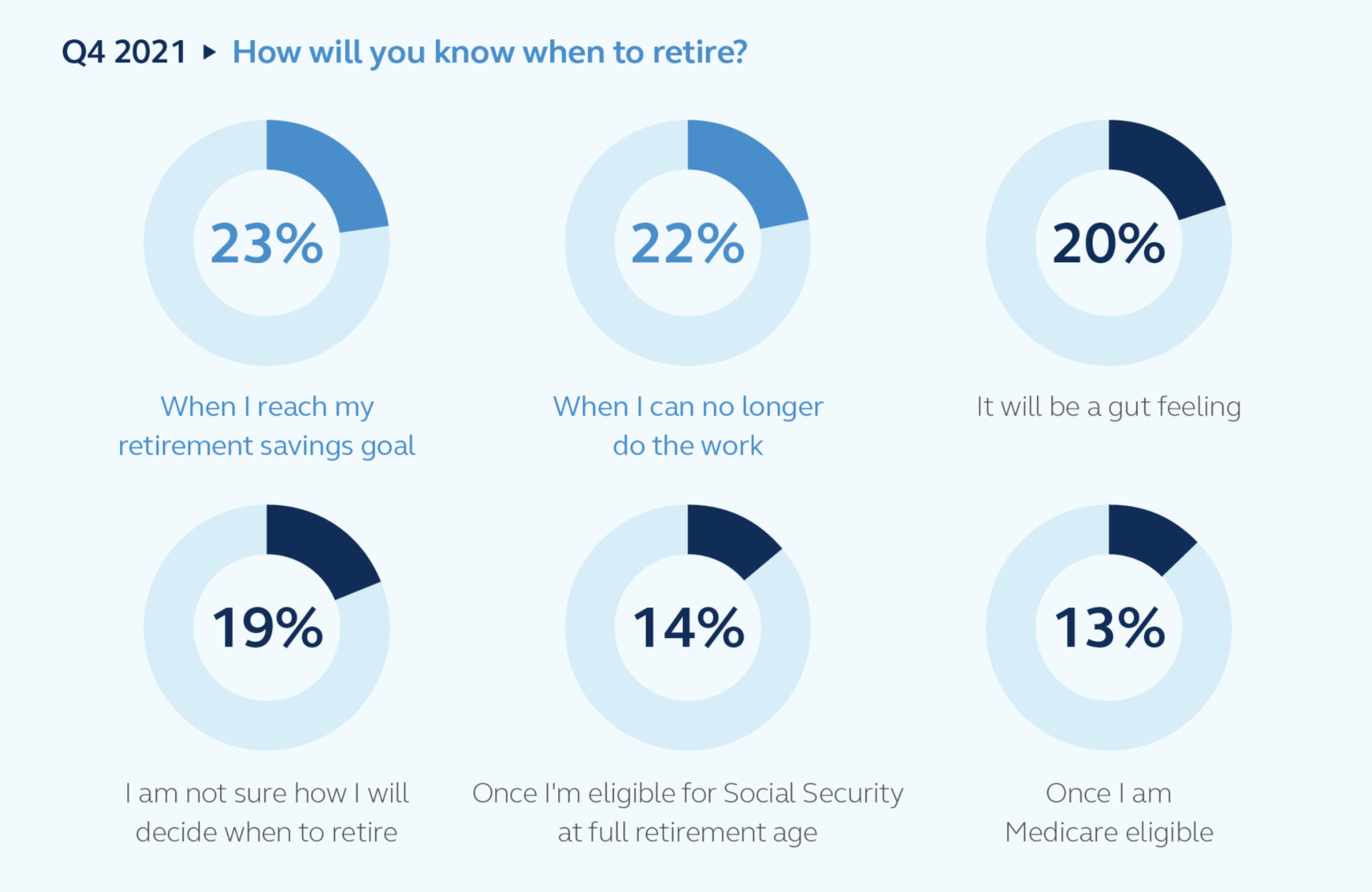

The following findings offer deeper insights into what workers, retirees, and plan sponsors are experiencing related to retirement planning and financial well-being.

Labor unions are working people’s greatest advocates. “Unions help ensure working people earn decent pay and benefits and have a voice in American democracy,” writes Dorian Warren , president at Community Change. To accomplish this, unions lobby and negotiate on behalf of workers to secure workplace safeguards and benefits that ensure workers are protected and treated fairly on the job. They fight for: Fair compensation. Paid family leave for all workers. Reskilling and training opportunities for workers. Health and safety protections in the workplace. Pension and retirement benefits. Workers’ compensation after on-the-job injuries. The last one — workers’ compensation — is especially critical for workers. If they can’t work, they can’t earn money. They are also often at risk of losing their jobs because they are unable to perform their duties after an injury. Unions work to protect an injured worker’s income and job. Unions Offer Supplemental Benefits Workers’ compensation programs only pay a portion of a worker’s wages to them while they are out of work with an injury. That’s why unions offer supplemental benefits to workers who are injured on the job. Through such funds, like the United Federation of Teachers (UFT) Welfare Fund and the Social Service Employees Union (SSEU) Local 371 Welfare Fund, workers who cannot work due to workplace injury can receive disability benefits to help them with their finances while out of work. These welfare funds provide safety nets such as cash stipends, weekly or monthly short-term and long-term disability benefits, and pension benefits in the case of an early retirement due to injury. Such assistance is invaluable for members because it helps fill the financial gaps workers face when their pay is cut. Union Contracts Include Job Protections for Workplace Injuries Union workers often have different workers’ compensation benefits than nonunion workers. Collective bargaining agreements often dictate specific workers’ compensation benefits members are entitled to receive if injured on the job. While these benefits may be similar to those provided under state law, they usually include member-specific benefits. In some states, legislation supports unions and management working together to create their own workers’ compensation programs through collective bargaining. For example, construction industry employers and unions in Minnesota developed the Union Construction Workers’ Compensation Program (UCWCP) that allows injured workers to forgo the state-run system and seek assistance through pre-approved providers. This keeps the focus on “recovery and return to the trade whenever possible,” assert the leaders of the UCWCP . Focusing on workers’ compensation benefits and programs in negotiations ensures workers have the protection they need should they get hurt at work. Union Stewards Assist Injured Workers Post-Accident The big question all workers have after they are injured on the job is “what next?”. Those that are union members are going to, rightfully, turn to their union stewards to help them navigate the next steps. Union representatives can help injured members by: Arranging immediate medical care after the accident. Assisting them with filing their workers’ compensation claims. Informing them about any supplemental benefits and how to apply for them. Strengthening the member’s case by finding witnesses and collecting evidence. Holding management accountable to terms set forth in a collective bargaining agreement. Representing the member’s interests throughout the process. Such a high level of involvement, assistance, and advocacy ensures workers are treated fairly after an accident and collect all the benefits they’re entitled to. Not all employers are concerned with their employees’ well-being after an accident. Getting the job done is often a greater priority than protecting workers before and caring for them after an injury. That’s why unions are such staunch advocates for workers’ compensation benefits. Union leaders understand the obstacles workers face when injured on the job and have the resources to mitigate those challenges by providing supplemental benefits, negotiating workers’ compensation benefits in contracts, and assisting workers after a workplace accident. Communication is critical at a time like this. Unions can use a tool like UnionTrack ENGAGE to make it easier for members to engage with union leaders and work through the workers’ compensation process.